The move comes as the Bengaluru-based company looks to raise capital in the public markets amid intensifying competition in the 10-minute delivery segment, with a fresh set of rivals including Amazon and Flipkart doubling down.

According to people who attended investor meetings with Zepto’s senior management, the five-year-old company is targeting full-year post-tax profitability by FY2028-29, while continuing to grow at 25-30% quarter-on-quarter.

“Across the quick commerce space, growth does seem to be cooling off a bit, at least for the bigger players. But that’s not entirely surprising. It lines up with what public market investors want to see right now: a clearer focus on profitability and stronger bottom-line performance,” said one person, who did not wish to be identified.

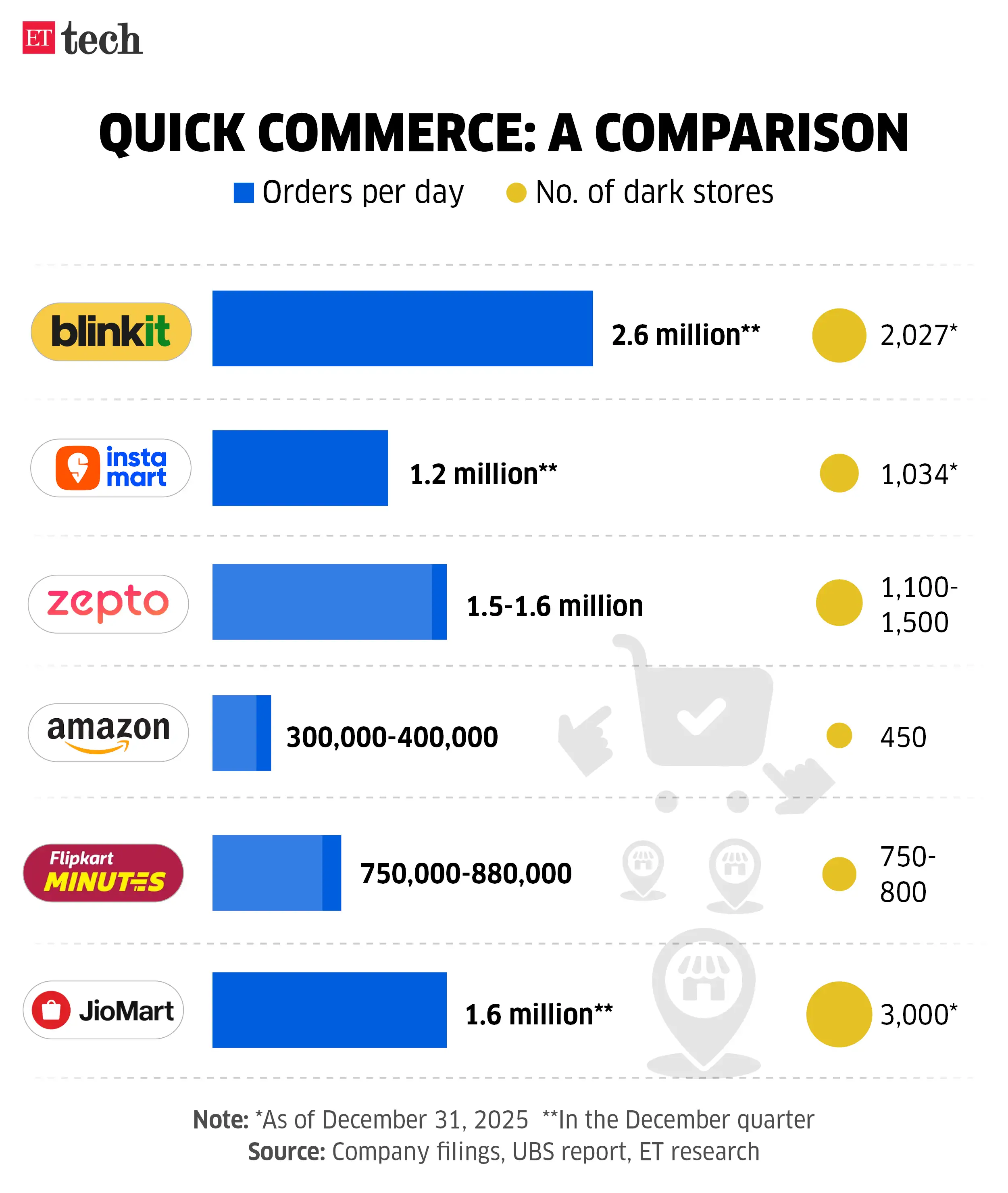

That person added that Zepto reduced its quarterly cash burn to Rs 850-900 crore in the January-March period, down from roughly Rs 1,200-1,300 crore a few quarters ago — driven by lower per-order costs and a pullback in network expansion, with its dark store count holding at around 1,100.

ETtech

ETtech

“The company has also outlined a path to profitability by FY29, with breakeven expected in FY28,” said another person familiar with the presentations.

In the quarter ended March 2026, Zepto reported an Ebitda loss of around Rs 55-60 crore, down from roughly Rs 100-110 crore in the July-September period. Editda measures earnings before the impact of financing costs, taxes, and certain non-cash accounting charges.

Zepto has confidentially filed draft papers for a Rs 11,000–12,000 crore IPO, largely comprising a primary issuance. The final size and pricing, however, remain undecided as the company awaits clearance from the country’s stock market regulator. Sebi.

Zepto’s push toward profitability mirrors moves by rivals Blinkit and Swiggy’s Instamart. In October-December 2025, Eternal-owned Blinkit reported breakeven at an adjusted Ebitda level, while flagging competitive intensity as a drag on margins. Swiggy, during the same period, said it would avoid “irrational” tactics such as zero delivery fees and handling charges. Instamart has guided for contribution margin breakeven in the ongoing April-June quarter.

Zepto did not respond to a detailed set of queries sent by ET.

Also Read: Ecommerce, quick commerce chasing ad spends with profitability in focus

The growth pitch

At a time when overall quick commerce growth is moderating and platforms are reining in investment, Zepto is making the case for scaling order volumes without significantly expanding its dark store network.

In a recent note, UBS said quick commerce growth is slowing due to both seasonality and a shift by larger platforms such as Blinkit and Instamart toward balancing growth and margins.

“Zepto’s footprint of around 1,100 dark stores has remained largely unchanged since late last year, but order volumes have grown,” said one of the people cited earlier. “In the January–March period, it claims to have clocked 2.4–2.5 million orders per day on average, growing 25–30% sequentially, driven by discounts and schemes that bring in new customers.”

Zepto is trying to differentiate itself from larger rival Blinkit by targeting more value-conscious customers. “In retail, DMart attracts higher footfall than mid-premium or premium offline players. Even with lower price points, the volumes help make the unit economics work — that is Zepto’s play against Blinkit, which plays to its strengths of a wider assortment and better serviceability,” one person said.

An investor who reviewed the company’s presentations said Zepto’s claim of reducing supply chain costs by 20–25% over the past few quarters to about Rs 90–95 per order is largely a function of higher throughput at its dark stores.

“Last quarter, it said it was clocking over 2,100–2,200 orders per day per dark store,” the person said. “The biggest lever for reducing per-order costs is pushing more volume through each store.”

Also Read: Quick commerce expands beyond groceries with VC funding, but scale questions persist

Valuation concerns persist

Zepto last raised $450 million in October 2025 at a $7 billion valuation. However, institutional investors ET spoke to said that figure now appears out of step with current public market conditions.

“On a year-to-date basis, Eternal’s stock is down about 15–20%, while Swiggy is down 25–30%. In that environment, there will always be questions around how much the company can raise,” one investor said. “Some companies have delayed IPOs to get the valuations they want — but now Eternal and Swiggy, where markets have clearer visibility on metrics, are also available at cheaper valuations.”

In March, Walmart-owned PhonePe deferred its IPO plans after receiving regulatory approval due to a mismatch in valuation expectations, ET had reported.