The expected slowdown comes alongside intensifying competition, with Amazon and Flipkart stepping up their presence in the segment. Rival Zepto, which is targeting a June-July listing, is also increasingly emphasising profitability in its pitch to public market investors, ET reported on April 14.

“Growth is starting to taper off for most large players,” a senior industry executive said. “We’re seeing early signs of saturation in bigger markets and competition from existing quick commerce players is also beginning to bite.”

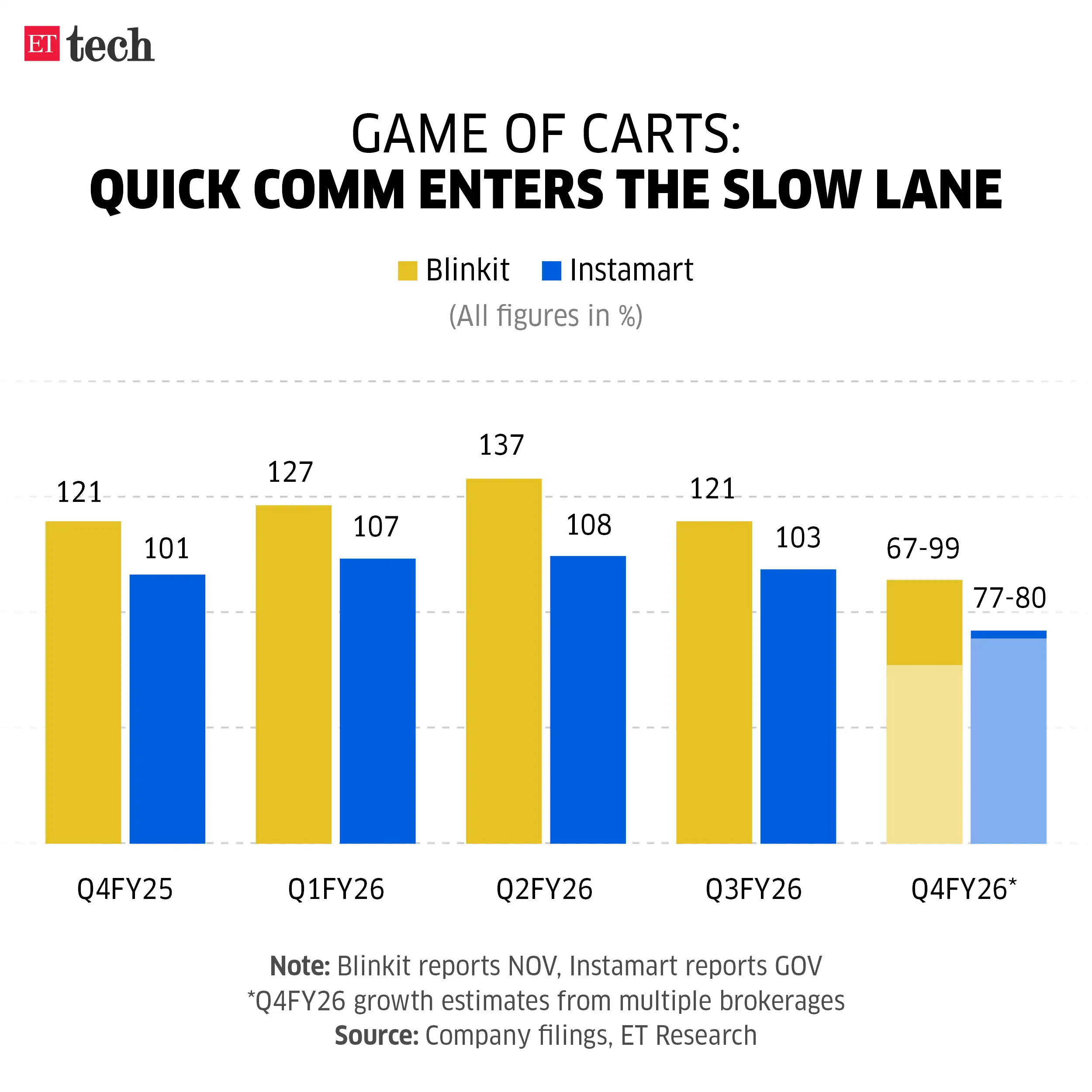

Brokerages estimate Eternal-owned Blinkit to report 67-99% net order value (NOV) growth for the March quarter from a year earlier, a step down from the over 100% growth it sustained over the previous six-seven quarters.

Instamart, which had reported a sequential drop in order volumes in the December quarter, is expected to post gross order value (GOV) growth of 77-80%, compared with consistently doubling this metric on a yearly basis earlier.

During the third quarter of FY26, Blinkit reported NOV of Rs 13,300 crore, up 121% year-on-year. Instamart, which reports GOV, posted Rs 7,938 crore in gross sales, up 103%. NOV is GOV minus discounts.

ETtech

ETtechAnalysts say rising competitive intensity has begun to weigh on growth trajectories, even as the market remains underpenetrated. “While we expect Blinkit’s share gains versus Swiggy to continue, its growth may have been adversely impacted in recent months due to elevated competition from both new entrants and existing players,” Goldman Sachs said in a report.

Some investors have flagged concerns around Blinkit’s medium-term growth outlook, the brokerage said. “In our recent investor conversations, we have heard concerns that Blinkit’s FY27 NOV growth could fall below 50% in a bear case, given the current quarter-on-quarter growth run rate,” it said, adding that it sees such a scenario as low probability given the still early-stage total addressable market. However, risks remain if basket sizes stay range-bound or competitive intensity persists, it pointed out.

During the October-December quarter, Blinkit just about broke even at an adjusted Ebitda level, posting an operating profit of Rs 4 crore.

Instamart continued to post heavy losses—Rs 908 crore at the adjusted Ebitda level for the December quarter—dragging the bottom line of parent Swiggy, which, like Eternal, has a profitable food delivery business.

At Instamart, growth pressures have been visible at the lower end of the market. The company had earlier flagged a decline in order volumes among price-sensitive users, attributing it to what it described “irrational competition”. Swiggy’s management had indicated that it would prioritise profitability even at the cost of near-term order growth.

Brokerages expect early signs of margin improvement as companies pull back on aggressive discounting.

BofA Securities said despite Instamart rolling back its earlier free delivery offering, volumes are unlikely to be materially impacted. It expects a marginal improvement in contribution margins, along with a slight reduction in losses. Swiggy has guided for Instamart to turn contribution-margin positive by the ongoing April-June quarter.

UBS said while competition remains intense in the near term, it has not worsened compared with the December-January period. It pointed to measures such as higher thresholds for free delivery and improved discount discipline as factors that would have supported margins in the March quarter.

Growth moderation reflects a combination of seasonality and a more calibrated approach by Blinkit and Instamart as they balance expansion with profitability, it said.